Roth Conversion Ladder: Complete Guide for Early Retirees

What Is a Roth Conversion Ladder?

A Roth conversion ladder is the primary strategy for early retirees to access pre-tax retirement funds (Traditional IRA, 401(k), 403(b)) before age 59½ without paying the 10% early withdrawal penalty. Under IRS Publication 590-B, converted amounts (not earnings) can be withdrawn penalty-free after a 5-year seasoning period, regardless of the account holder's age. This rule is the foundation of the entire strategy.

A Roth conversion ladder is the primary strategy for early retirees to access pre-tax retirement funds (Traditional IRA, 401k) before age 59½ without paying the 10% early withdrawal penalty. You convert a portion each year, pay ordinary income tax on the conversion amount, then withdraw the converted principal penalty-free after a 5-year seasoning period. The key insight is that Roth conversions (not earnings) can be withdrawn after 5 years regardless of your age.

The strategy works because of a specific IRS rule: while Roth IRA earnings can't be withdrawn tax- and penalty-free until age 59½, Roth conversion amounts follow a different rule. Each conversion has its own 5-year clock. Once 5 years have passed from the conversion, you can withdraw that converted amount without penalty, even if you're 45 years old.

This creates a "ladder": each year's conversion becomes accessible 5 years later, creating a steady stream of penalty-free income.

How the 5-Year Ladder Works

The 5-year seasoning rule means each conversion has its own independent clock. A conversion made on January 2, 2026, becomes available for penalty-free withdrawal on January 1, 2031, exactly 5 tax years later. During those 5 years, you need to fund your living expenses from other sources: taxable brokerage accounts, existing Roth contributions (which can always be withdrawn tax- and penalty-free), cash, or part-time Coast FIRE income.

The Roth conversion ladder requires advance planning because of the 5-year seasoning requirement. You need enough money outside of pre-tax retirement accounts to cover 5 years of living expenses while the first rungs of the ladder mature. This typically comes from taxable brokerage accounts, existing Roth contributions (not conversions), cash savings, or part-time income during a Coast FIRE phase.

Here's a concrete timeline for someone retiring at age 40:

| Year | Age | Action | Available for Withdrawal |

|---|---|---|---|

| 2026 | 40 | Convert $50,000 from Traditional IRA to Roth | Live on taxable account |

| 2027 | 41 | Convert $50,000 | Live on taxable account |

| 2028 | 42 | Convert $50,000 | Live on taxable account |

| 2029 | 43 | Convert $50,000 | Live on taxable account |

| 2030 | 44 | Convert $50,000 | Live on taxable account |

| 2031 | 45 | Convert $50,000 | Withdraw 2026 conversion ($50,000) |

| 2032 | 46 | Convert $50,000 | Withdraw 2027 conversion ($50,000) |

| ... | ... | Continue | Continue |

After the initial 5-year bridge period, you have a self-sustaining pipeline: each year you convert another rung, and each year a 5-year-old rung becomes available for withdrawal.

Optimal Conversion Amounts: Bracket Filling

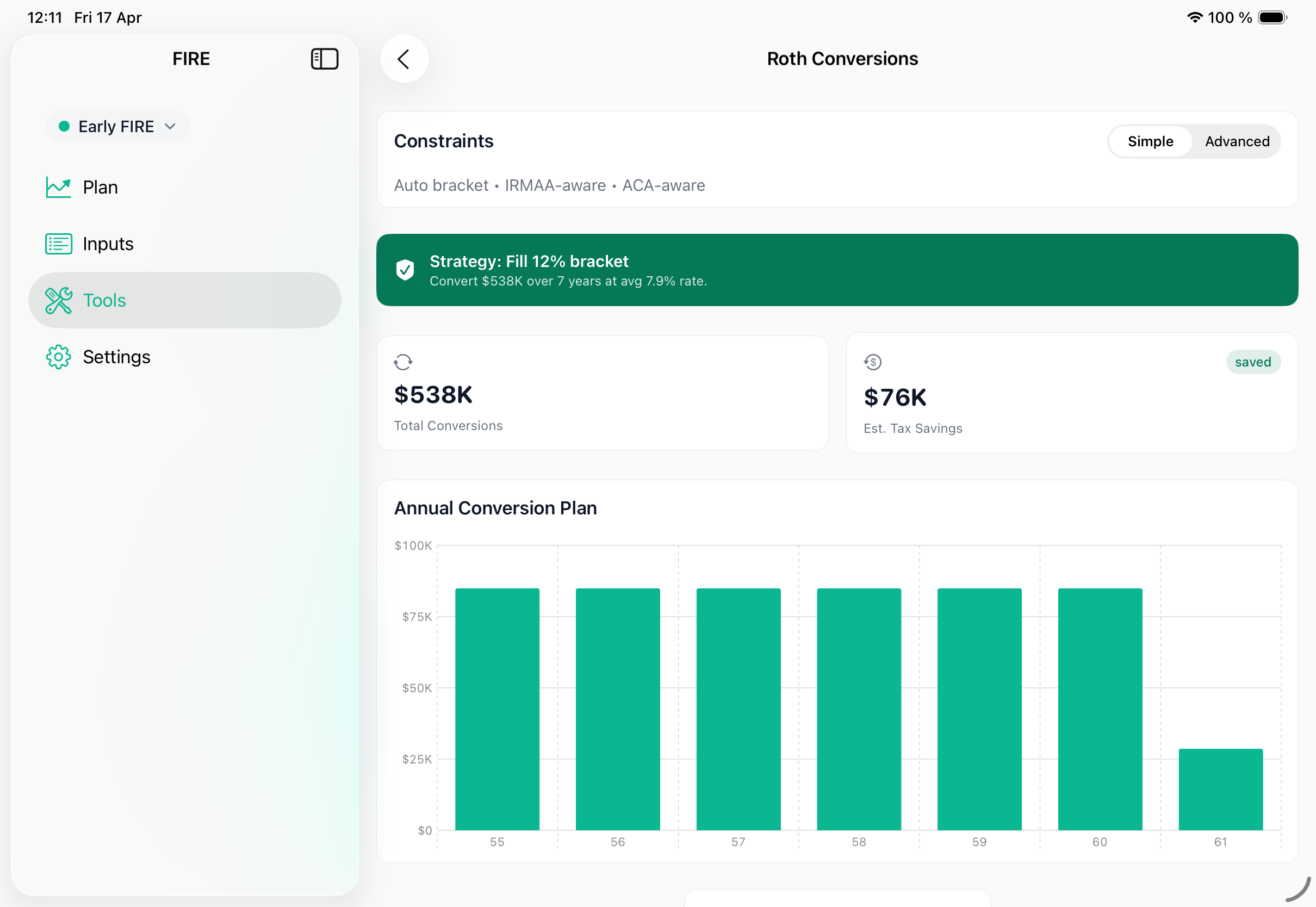

The most tax-efficient approach is "bracket filling": converting exactly enough each year to use up the lowest federal tax brackets without spilling into the next one. Per IRS Revenue Procedure 2024-40, the 2025 MFJ brackets are 10% up to $23,200 and 12% up to $94,300 of taxable income. After the $30,000 standard deduction, that means a couple can convert up to $124,300 and stay entirely within the 10% and 12% brackets.

The most tax-efficient Roth conversion strategy is "bracket filling": converting exactly enough each year to fill up the lowest tax brackets without spilling into higher ones. For a married couple with no other income in 2025, converting up to $124,300 keeps all income in the 10% and 12% brackets after the $30,000 standard deduction. Converting even $1 more pushes that dollar into the 22% bracket, nearly doubling the marginal rate.

2025 Bracket-Filling Targets (Married Filing Jointly)

| Strategy | Conversion Amount | Taxes Paid | Effective Rate |

|---|---|---|---|

| Fill 0% (standard deduction only) | $30,000 | $0 | 0% |

| Fill 10% bracket | $53,200 | $2,320 | 4.4% |

| Fill 12% bracket | $124,300 | $10,852 | 8.7% |

| Fill 22% bracket | $231,050 | $34,337 | 14.9% |

For most early retirees, filling the 12% bracket is the sweet spot. The jump from 12% to 22% is the largest single-bracket increase in the tax code. Converting at 12% when your future RMDs would force withdrawals at 22-24% is a guaranteed tax savings.

Why This Beats Waiting for RMDs

Without Roth conversions, your Traditional IRA continues to grow tax-deferred. When Required Minimum Distributions (RMDs) start at age 73 (under SECURE 2.0), you are forced to withdraw, and those withdrawals are taxed as ordinary income.

Example: $1 million Traditional IRA at age 50, growing at 7% nominal:

- At age 73: approximately $4.7 million

- First RMD (age 73, ~3.8%): approximately $178,600

- Tax on $178,600 (MFJ, 2025 brackets): approximately $27,400 (15.3% effective)

If instead you converted $100,000/year from ages 50-60 at an 8.7% effective rate, you'd pay roughly $87,000 total in conversion taxes but save far more in avoided RMD taxes over the following decades.

The ACA Subsidy Cliff Trap

The ACA premium tax credit is the single biggest constraint on Roth conversion sizing for pre-Medicare retirees. Under Healthcare.gov guidelines, exceeding 400% of the Federal Poverty Level ($78,880 for a household of 2 in 2025) eliminates all premium subsidies, a cliff that can cost $15,000-$25,000 in a single year. This risk is why every Roth conversion calculator must model ACA interactions, and why most retirement calculators get taxes wrong.

The single biggest risk in Roth conversion planning is accidentally exceeding the ACA (Affordable Care Act) income threshold and losing all health insurance premium subsidies. In 2025, a married couple losing ACA subsidies at the cliff can face $15,000-$25,000 in additional annual healthcare costs. This can completely negate the tax savings from the conversion. Any Roth conversion strategy for pre-Medicare retirees (under age 65) must account for this interaction.

The ACA premium tax credit phases out when your Modified AGI exceeds 400% of the Federal Poverty Level (FPL). For a household of 2 in 2025, that's approximately $78,880. Roth conversions count toward MAGI.

This creates a hard constraint: your total income (including Roth conversions) should stay below ~$78,880 if you're relying on ACA subsidies. For a couple with $20,000 in other income, that limits Roth conversions to roughly $58,000/year.

A tax-aware conversion optimizer models this constraint directly by calculating the maximum conversion that keeps you below the ACA cliff, comparing the tax savings of a larger conversion against the lost subsidy, and recommending the optimal amount for each year.

IRMAA Interactions (Age 63+)

For retirees approaching Medicare age (65), Roth conversions done at ages 63+ can trigger IRMAA (Income-Related Monthly Adjustment Amount) surcharges on Medicare premiums. IRMAA uses income from two years prior, so a large conversion at age 63 increases your Medicare premiums at age 65. The surcharges range from $1,000 to $6,000+ per person per year and create additional cliff effects that must be modeled alongside conversion strategy.

The IRMAA thresholds for 2025 (based on 2023 income):

| MAGI (MFJ) | Part B Monthly Surcharge (per person) | Annual Impact (couple) |

|---|---|---|

| ≤ $206,000 | $0 | $0 |

| $206,001 - $258,000 | $70.00 | $1,680 |

| $258,001 - $322,000 | $175.00 | $4,200 |

| $322,001 - $386,000 | $280.00 | $6,720 |

| $386,001 - $750,000 | $384.90 | $9,238 |

| > $750,000 | $419.30 | $10,063 |

Going $1 over the $206,000 threshold costs $1,680/year. This is a pure cliff with no phase-in. Any retirement calculator modeling Roth conversions for ages 63+ must flag these thresholds.

Coordinating With Other Income Sources

The optimal Roth conversion amount is not a fixed number; it changes every year based on your other taxable income sources. Each dollar of pension, Social Security, or capital gains that fills a tax bracket is a dollar that can't be used for a low-rate conversion. This interaction between income sources is the primary reason a Roth conversion strategy requires annual recalculation, not a one-time plan.

- Social Security benefits: If you have started claiming, up to 85% is taxable income that reduces your conversion room

- Pension income: Fully taxable as ordinary income, directly reduces bracket space

- Part-time employment: Earned income fills brackets and subjects you to FICA

- Capital gains harvesting: If you are also harvesting capital gains from a taxable account, the gains stack on top of conversions for bracket purposes

- RMDs: Once RMDs start (age 73), they fill brackets before you can convert. This is why converting before RMDs begin is so valuable

A tax-aware retirement calculator must model all of these interactions simultaneously, producing a year-by-year plan with the optimal conversion amount given all your income sources, tax brackets, ACA constraints, and IRMAA thresholds.

Step-by-Step: Setting Up Your Roth Conversion Ladder

-

Roll your 401(k) into a Traditional IRA. You cannot do partial Roth conversions from a 401(k) at most employers. Roll it into a Traditional IRA first (this is not a taxable event).

-

Calculate your 5-year bridge. Determine how much you need annually for living expenses. Multiply by 5. This is how much you need accessible outside of pre-tax accounts.

-

Identify your bridge funding. Taxable brokerage accounts, existing Roth contributions (not conversions; original contributions can always be withdrawn tax- and penalty-free), cash, or part-time income during a Coast FIRE phase.

-

Determine your annual conversion target. Use a Roth conversion optimizer or manually calculate your bracket-filling amount based on other income and the ACA/IRMAA constraints above.

-

Execute the conversion. Contact your brokerage. Most allow you to do this online. Convert from Traditional IRA to Roth IRA. You'll receive a 1099-R for tax reporting.

-

Pay taxes from non-retirement funds. Pay the tax on the conversion from your taxable account, not from the converted amount. Paying from the Roth account itself reduces the amount that compounds tax-free.

-

Repeat annually. Each January, evaluate your income situation and calculate that year's optimal conversion. Adjust as needed.

When Not to Do Roth Conversions

Roth conversions are not universally beneficial:

- If you expect to be in a higher bracket now than in retirement: Converting at 24% now to avoid 12% later is a bad trade

- If you will need the tax money from the conversion within 5 years: The 5-year rule means the conversion tax comes out of your bridge fund

- If you have very large RMDs but also very large expenses: If your RMDs will be offset by high spending, the effective tax rate on RMDs may not be much higher than conversion rates

- If your state taxes conversions but you plan to move to a no-tax state: Converting in California (13.3%) when you plan to retire in Texas (0%) wastes the state tax savings

The Bottom Line

A Roth conversion ladder is the most powerful tax optimization tool available to early retirees with pre-tax retirement accounts. It converts future high-bracket RMD taxes into current low-bracket conversion taxes, while simultaneously creating penalty-free access to funds before age 59½. The strategy requires a 5-year bridge, careful bracket management, and coordination with ACA subsidies and IRMAA thresholds. Lifetime tax savings typically run to six figures.

CoastIQ's Roth Conversion Optimizer handles this complexity. Enter your accounts, income sources, and target retirement age, and it generates a year-by-year plan that maximizes after-tax wealth while respecting all the constraints above. The Tax Analytics view then shows the lifetime tax impact of the conversion strategy versus doing nothing.

Frequently Asked Questions

Vlad Kuzin

Founder of CoastIQ. Building the most tax-accurate retirement calculator on iOS.