Coast FIRE Calculator: When Can You Stop Saving?

What Is Coast FIRE?

Coast FIRE is the point at which your existing retirement savings will grow, through compound returns alone with zero additional contributions, to fully fund your retirement by your target age. Once you cross this threshold, you no longer need to save for retirement. You only need to earn enough to cover your current living expenses.

The concept comes from the broader FIRE (Financial Independence, Retire Early) movement, but it's distinctly different from traditional FIRE. While full FIRE requires accumulating 25x your annual expenses before you can stop working entirely, Coast FIRE only requires that your investments have enough runway to compound their way to that number.

This distinction matters enormously. A 30-year-old who needs $1.5 million at age 60 doesn't need $1.5 million today. They need roughly $347,000 — the present value of $1.5 million discounted at a 5% real return over 30 years. That's the Coast FIRE number.

The Coast FIRE Formula

Coast FIRE Number = Target Retirement Portfolio / (1 + Real Return Rate) ^ Years Until Retirement. This formula calculates the present value of your future retirement need, discounted by the expected real (inflation-adjusted) rate of return on your investments.

Let's break down each variable:

Target Retirement Portfolio: This is how much you'll need at your retirement age to sustain your lifestyle. The standard FIRE formula uses 25x your annual expenses (based on the 4% rule from the Trinity Study). If you expect to spend $60,000/year in retirement, your target is $1,500,000.

Real Return Rate: The inflation-adjusted return on your investments. Historical US stock market real returns average roughly 7% nominal / 5% real. Most Coast FIRE calculators use 5-7%. The higher the rate you assume, the lower your Coast FIRE number — but the more risk you're taking that the future won't match the past.

Years Until Retirement: The gap between your current age and when you plan to start withdrawing. More years = more compounding = lower Coast FIRE number.

Example Calculations

| Current Age | Retirement Age | Years | Target Portfolio | Real Return | Coast FIRE Number |

|---|---|---|---|---|---|

| 25 | 60 | 35 | $1,500,000 | 5% | $271,000 |

| 30 | 60 | 30 | $1,500,000 | 5% | $347,000 |

| 35 | 60 | 25 | $1,500,000 | 5% | $443,000 |

| 40 | 60 | 20 | $1,500,000 | 5% | $565,000 |

| 30 | 65 | 35 | $2,000,000 | 5% | $362,000 |

The power of compounding is dramatic. A 25-year-old needs $76,000 less than a 30-year-old for the same retirement target. That is five extra years of compound growth doing the work.

Why Single-Point Estimates Are Dangerous

Using a single expected return rate for Coast FIRE calculations gives you a false sense of precision. Markets do not return 7% every year. They return -37% one year and +26% the next. The sequence of those returns matters enormously, and only Monte Carlo simulation captures that reality.

The standard Coast FIRE formula assumes your investments will grow at a constant rate every year. This has never happened in market history. The S&P 500's annual returns since 1928 range from -43.8% (1931) to +52.6% (1954), according to NYU Stern's historical data.

What matters isn't just the average return but the sequence of returns. Two portfolios with identical average returns over 30 years can end up with wildly different final values depending on when the bad years hit.

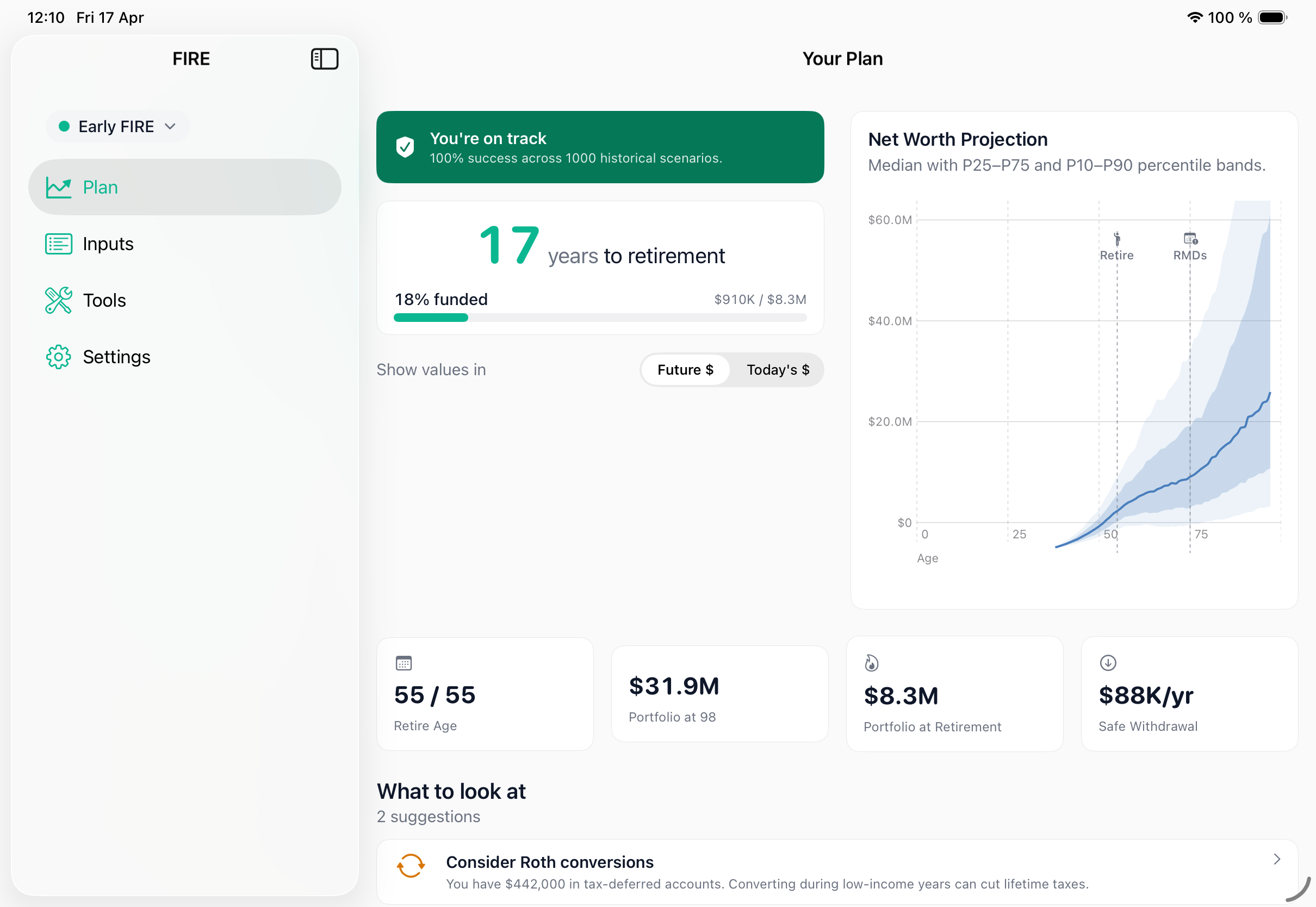

This is why Monte Carlo simulation with 1,000+ parallel trials matters more than a single-point formula. Instead of telling you "you need $347,000," it tells you "with $347,000, you have a 78% probability of reaching your target." That probability-based framing is far more useful for real decisions.

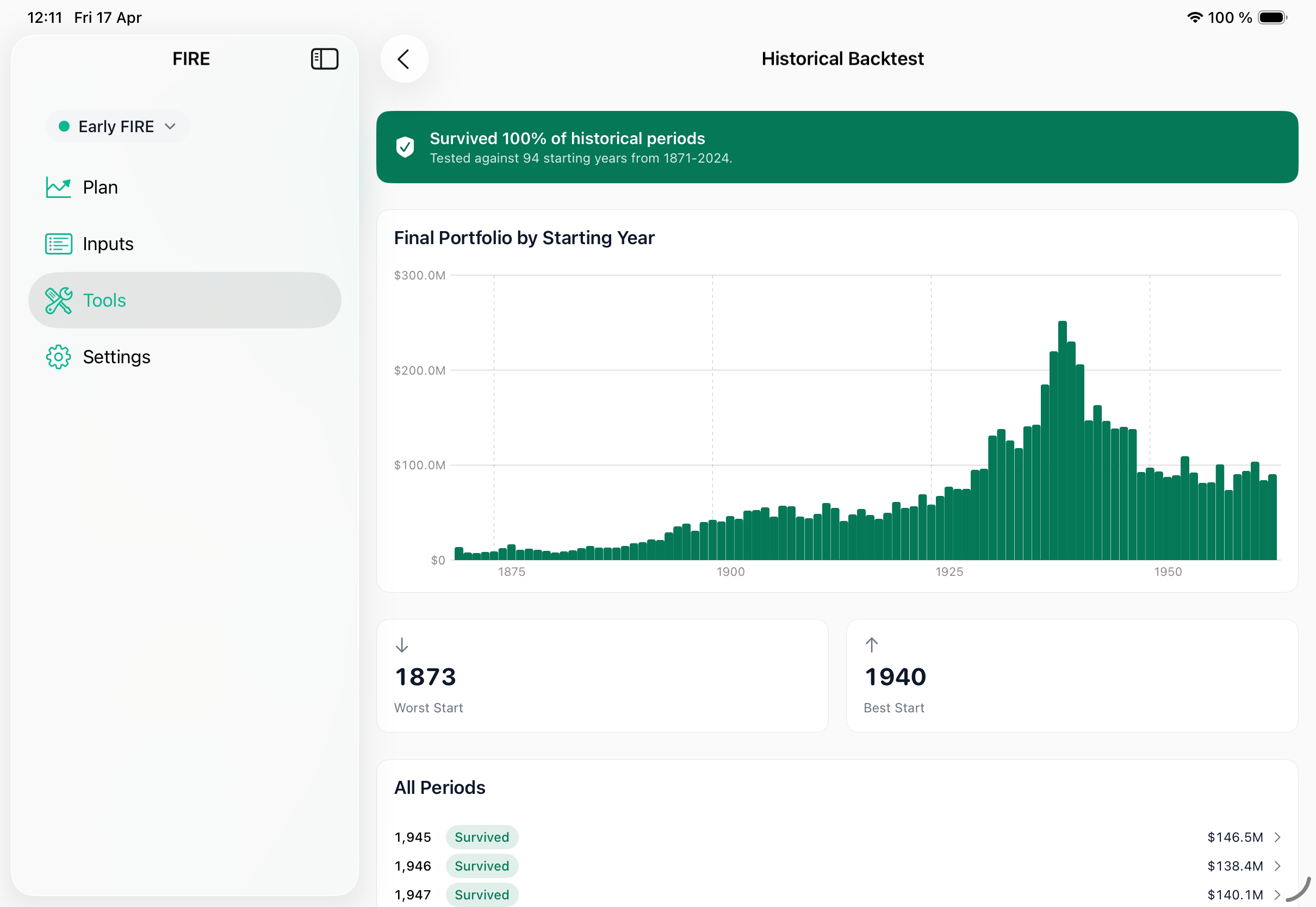

Historical Backtest vs. Monte Carlo

A rigorous Coast FIRE calculator should offer both approaches:

- Historical Backtester: Tests your scenario against every starting year from 1928 to today. Shows you the actual worst case (starting in 1929 or 2000) and best case.

- Monte Carlo Simulation: Generates 1,000+ randomized return sequences based on historical distributions, including correlated stock and bond returns. Shows you a probability distribution with P10, P50, and P90 outcomes.

The historical backtest answers: "Would this have worked in the past?" Monte Carlo answers: "How likely is this to work in the future?" Both are valuable, but Monte Carlo is more honest about uncertainty.

The Tax Problem Most Calculators Ignore

Most Coast FIRE calculators treat your portfolio as one big number, ignoring that a dollar in a 401(k) is worth less than a dollar in a Roth IRA after taxes. Your Coast FIRE number should be calculated on an after-tax basis, accounting for the different tax treatment of each account type.

Here's what most calculators get wrong:

Pre-tax accounts (401k, Traditional IRA): Every dollar you withdraw is taxed as ordinary income. If you're in the 22% federal bracket and live in California (9.3% state), your $1.5M 401(k) is really worth about $1.03M after taxes. Your Coast FIRE number based on the pre-tax balance is misleadingly low.

Roth accounts: Withdrawals are tax-free (after age 59½ with a 5-year holding period). A dollar in a Roth is worth a full dollar.

Taxable brokerage accounts: You pay capital gains tax on the growth, but only the growth. If your cost basis is 50% of the current value, you'd owe tax on half. Long-term capital gains rates (0%, 15%, or 20%) are lower than ordinary income rates, but they still reduce your effective portfolio value.

Capital gains stacking: This is where it gets tricky and where most calculators fail completely. Your capital gains rate depends on your total taxable income, including Social Security benefits, pension income, and required minimum distributions (RMDs). A tax-aware calculator models this by stacking capital gains on top of ordinary income to determine the effective rate.

Account Type Impact on Coast FIRE Number

| Account Mix | Gross Portfolio | Effective Tax Rate | After-Tax Value | Adjusted Coast FIRE # |

|---|---|---|---|---|

| 100% Roth | $1,500,000 | 0% | $1,500,000 | $347,000 |

| 100% 401(k) | $1,500,000 | ~27% | $1,095,000 | $475,000 |

| 50/50 Mix | $1,500,000 | ~14% | $1,290,000 | $404,000 |

| 70% Taxable / 30% Roth | $1,500,000 | ~8% | $1,380,000 | $377,000 |

The difference between a 100% Roth portfolio and a 100% 401(k) portfolio is a $128,000 gap in your Coast FIRE number. That's years of additional saving if you ignore tax treatment.

Roth Conversion Ladders and Coast FIRE

If you plan to retire before 59½, a Roth conversion ladder is essential for accessing pre-tax retirement funds without penalties. The ideal time to execute conversions is during the "coast" phase, when you have stopped saving aggressively and your income (and tax bracket) may be lower.

Once you reach Coast FIRE and potentially shift to lower-paying but more fulfilling work, your income drops. This creates a window for Roth conversions at lower tax brackets. The optimal approach is to fill up lower brackets without pushing you into the next one, while also respecting ACA subsidy cliffs and IRMAA thresholds.

Calculating Your Coast FIRE Date

CoastIQ's Retirement Date Finder tool directly answers the Coast FIRE question: "When can I stop saving?" Enter your current accounts, expected contributions, and target retirement age, and the tool calculates the earliest age at which your success rate exceeds your confidence threshold — even with zero additional contributions after that point.

The One More Year tool complements this by showing exactly what one additional year of work buys you: how much your success rate improves, how much your safe spending increases, and whether the marginal year is worth it.

Steps to calculate your Coast FIRE number:

- Enter your current account balances (401k, Roth IRA, taxable, etc.)

- Set your expected annual expenses in retirement

- Set your target retirement age

- Run the Monte Carlo projection and note your success rate

- Remove all future contributions (set savings to $0)

- Re-run. If your success rate is still above 90%, you have already reached Coast FIRE.

- If not, use the Retirement Date Finder to find when you'll cross that threshold

Coast FIRE vs. Other FIRE Variants

| FIRE Variant | Definition | Typical Target | Work After? |

|---|---|---|---|

| Full FIRE | 25x annual expenses saved | $1.5M+ | No |

| Coast FIRE | Enough saved to compound to full FIRE | $250K-500K | Yes, cover current expenses |

| Lean FIRE | 25x minimal expenses | $600K-1M | No, but frugal lifestyle |

| Barista FIRE | Partial portfolio + part-time income | Varies | Yes, part-time |

| Fat FIRE | 25x generous expenses | $2.5M+ | No, premium lifestyle |

Coast FIRE is unique because it reframes the question. Instead of "when can I stop working?" it asks "when can I stop worrying about retirement savings?" For most FIRE pursuers, that psychological shift is the real value — the freedom to take a lower-paying job, start a business, or work part-time without worrying about retirement.

Common Coast FIRE Mistakes

Ignoring Inflation in Your Target

Your future expenses won't be today's expenses. If you're 30 and plan to retire at 60, and you spend $60,000/year today, you'll need roughly $109,000/year at 60 (assuming 2% inflation). That means your target portfolio is not $1.5M but $2.7M. Always use real (inflation-adjusted) returns or inflate your target.

Using Only Average Returns

As discussed above, average returns hide enormous variance. A Coast FIRE calculator that uses 7% nominal returns will tell you that you need less than one that uses Monte Carlo simulation with historical return distributions. The Monte Carlo version is more honest.

Forgetting About Healthcare

Before 65 (Medicare eligibility), you need to fund your own health insurance. ACA marketplace premiums depend on your Modified Adjusted Gross Income (MAGI). If you're doing Roth conversions during your coast phase, those count as income and can push you above ACA subsidy cliffs — a mistake that can cost $15,000-$25,000 in a single year.

Ignoring Social Security

Social Security benefits reduce how much you need from your portfolio. A couple expecting $40,000/year combined from Social Security at age 67 only needs their portfolio to cover the gap between total spending and Social Security income. This significantly lowers both your full FIRE number and your Coast FIRE number. Optimizing your claiming age can shift your Coast FIRE date by 2-3 years.

Frequently Asked Questions

Vlad Kuzin

Founder of CoastIQ. Building the most tax-accurate retirement calculator on iOS.